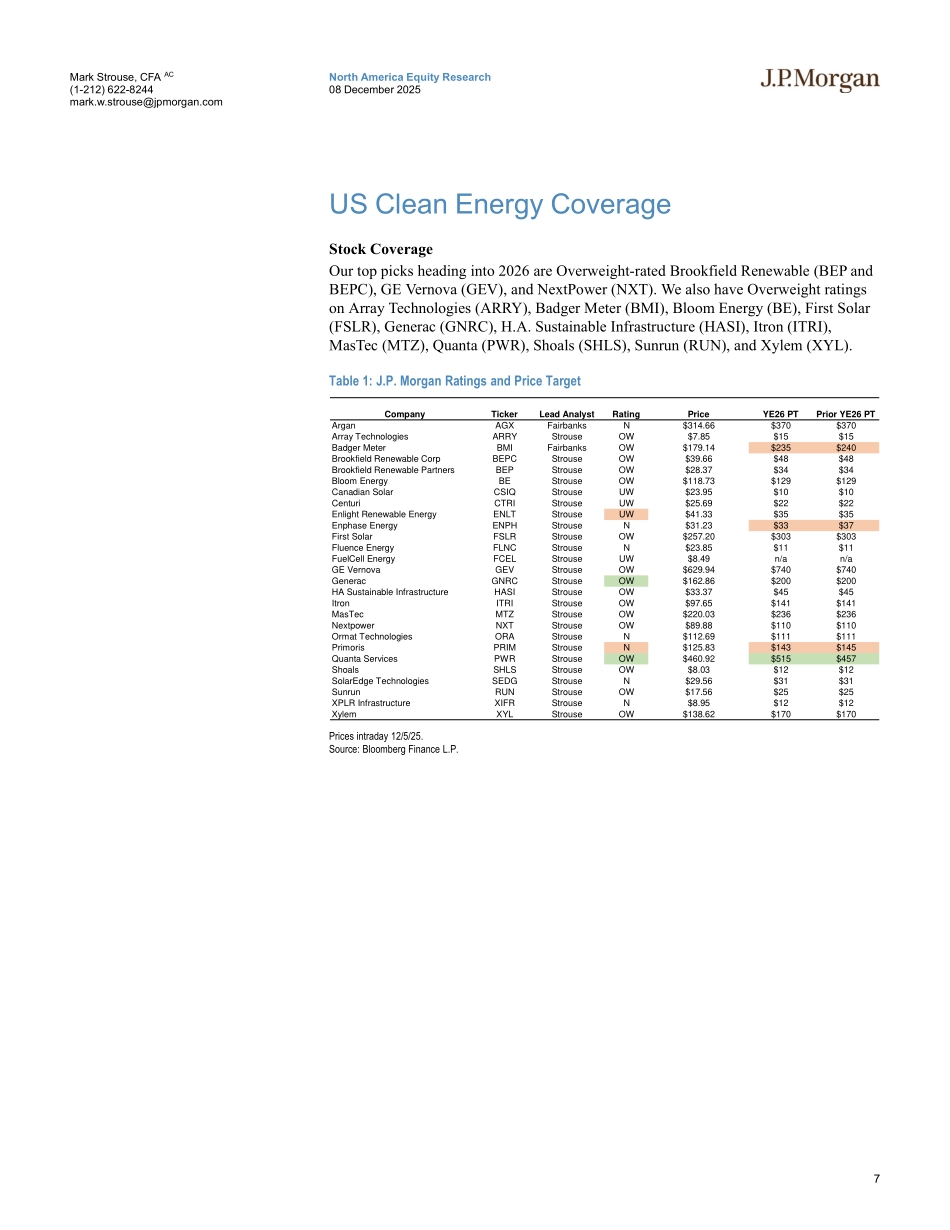

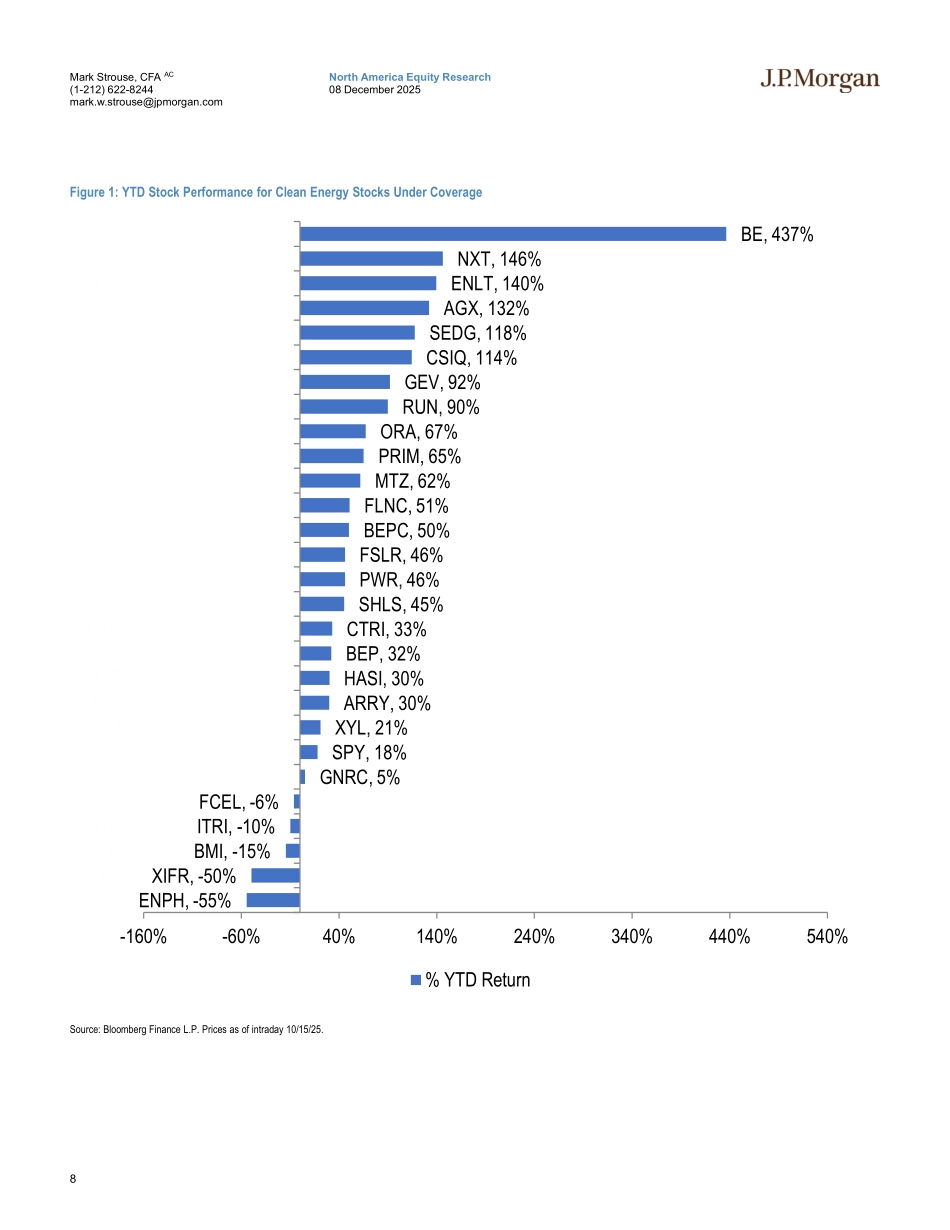

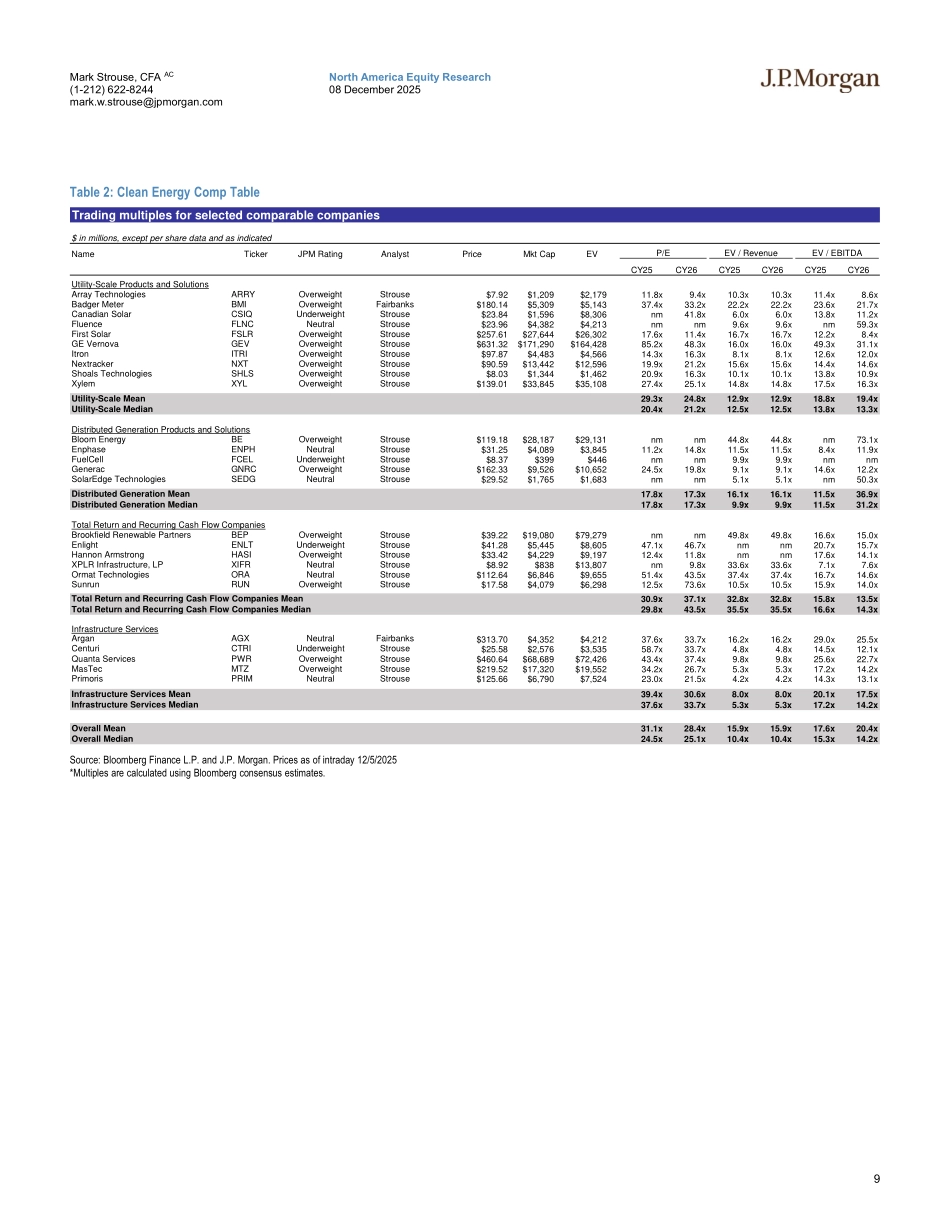

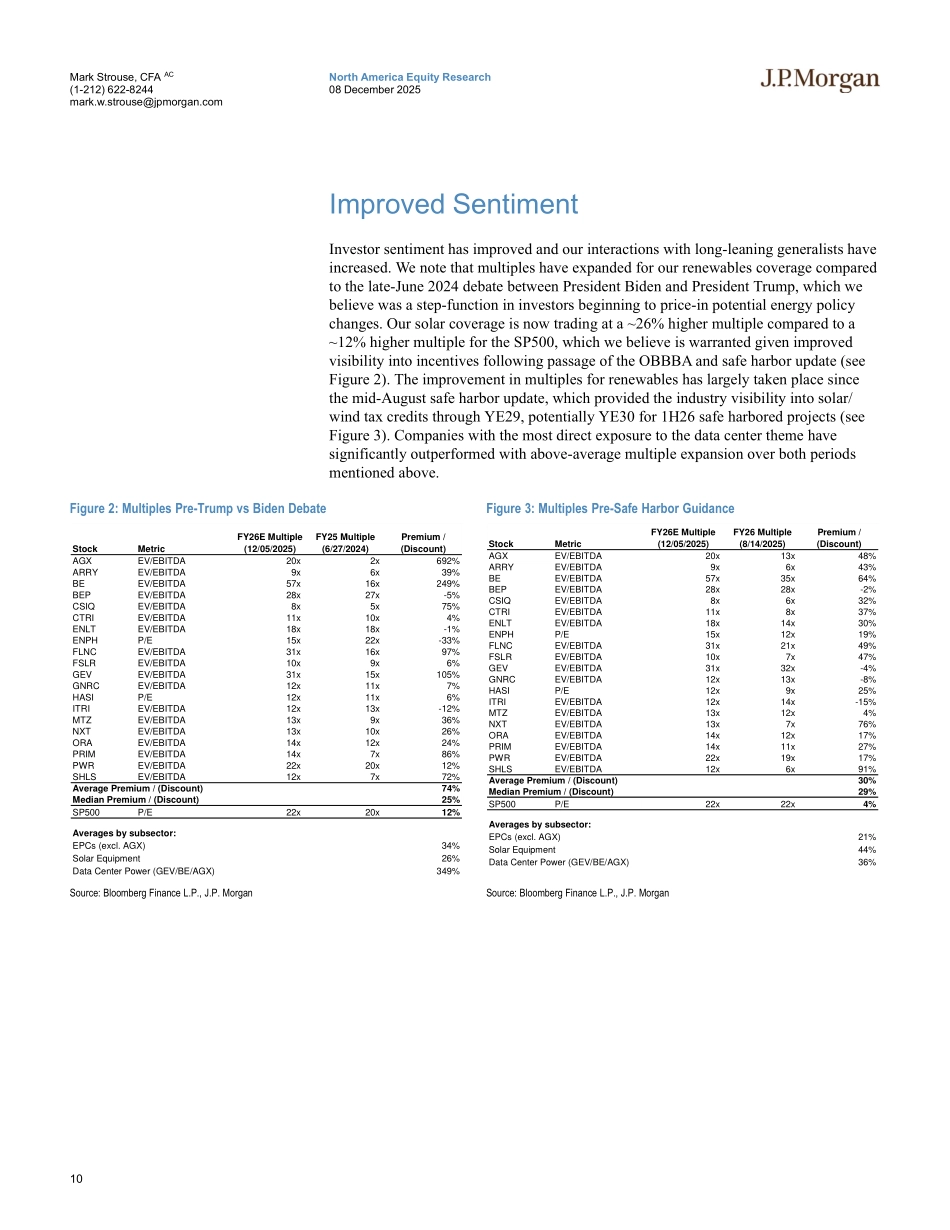

North America Equity Research08 December 2025J P M O R G A NClean Energy2026 Outlook: Back to Baseload Basics; Renewables Likely ConsolidateClean Energy / Sustainable InvestingMark Strouse, CFA AC(1-212) 622-8244mark.w.strouse@jpmorgan.comMichael G Fairbanks AC(1-212) 622-4908michael.fairbanks@jpmchase.comJ.P. Morgan Securities LLCAll pricing as of intraday December 05, 2025, unless otherwise noted.Heading into 2026, we expect baseload power sources to remain top of mind for investors, though we expect the thematic trade to become more nuanced by individual stock fundamentals and valuation, rather than simply by exposure. Within renewables, we expect another year of outperformance for the utility-scale market, though we expect a trend towards larger, more complex projects as well as a more complex regulatory environment to lead to consolidation of upstream and downstream providers, generally a tailwind for public companies in our coverage. While investor sentiment for renewables has improved and our interactions with long-leaning generalists have increased given improved US regulatory clarity and accelerating power demand, we note that there are potential risks still lingering such as initial FEOC guidelines, possible Department of Interior permitting delays, AD/CVD and/or Section 232 tariffs, etc. We therefore maintain our preference for stocks with significant exposure to U.S.-based manufacturing, diversified end markets, and/or strong balance sheets, including Overweight-rated BEP, GEV, and NXT. Lastly, with this note, we are shuffling our ratings somewhat, upgrading GNRC and PWR to Overweight, from Neutral, downgrading PRIM to Neutral from Overweight and ENLT to Underweight from Neutral. •Baseload power likely remains in focus though expect return to basics. We expect baseload power sources including CCGT, aeroderivative turbines, recip engines, fuel cells, BESS, and geothermal to experience accelerating order activity in 2026, driven by data centers, electrification of industry, and US manufacturing onshoring. That said, we expect company fundamentals and valuation to increasingly come back into focus, following outperformance of select stocks primarily owing to “exposure” to certain themes despite relatively lower order activity, pricing power, margins, etc. •Expect consolidation within renewables. We note that BNEF expects US utility scale solar to decline 13% y/y. However, industry checks with larger developers, manufacturers, and EPCs are generally more optimistic and point to firm backlog as evidence. We therefore believe the industry is ripe for consolidation as projects become larger and more complex (e.g. solar+storage instead of solar-only), and larger participants generally have stronger experience and financial wherewithal to adapt to changing policy regulations (e.g. compliance with safe harbor and FEOC). We view this as generally positive for companies...